Q1FY2020 Result Update| banking

July 30, 2019

ICICI Bank

BUY

CMP

`429

Decent Q1 with stable asset quality

Target Price

`490

Investment Period

12 Months

Particulars (` cr)

Q 1FY20

Q 4FY19

% chg (qoq)

Q 1FY19

% chg (yoy)

NII

7,737

7,620

2

6,102

27

Stock Info

Pre-prov. profit

6,288

6,233

1

5,808

8

Sector

Banking

PAT

1,908

969

97

(120)

-

Market Cap (` cr)

2,77,000

Source: Company

Beta

1.3

For Q1FY2020, ICICI Bank reported net profit of `1,908Cr, which is marginally

52 Week High / Low

444/282

lower than estimates primarily owing to decline in other income and higher

Avg. Daily Volume

6,60,886

provision. However, on asset quality front, bank reported improvement on all

Face Value (`)

2

parameters. Slippage for the quarter came in at `2,779Cr, which has been

BSE Sensex

37,686

witnessing a declining trend for last several quarters. Management has guided

Nifty

11,189

credit cost of 1.2-1.3% for FY2020 and 1% for FY2021.

Reuters Code

ICBK.BO

Bloomberg Code

ICICIBC IN

Stable asset quality and stressed pool declined: During the quarter, the key

monitorable was higher slippages from kisan credit card portfolio (`450cr), which

led the increase in retail GNPA ratio by ~20bps qoq to 1.9%. Key positives for the

quarter were (1) decline in BB & below book by 40bps to 2.59% of advances; on

Shareholding Pattern (%)

absolute basis it reduced by `2,170Cr, (2) Management mentioned that exposure

Promoters

0.0

to new stressed corporate was limited, (3) PCR at 73% was amongst the highest in

industry, and (4) delinquency in retail business is less than industry..

MF / Banks / Indian Fls

34.8

Advances led by retail lending; NIM stable : The bank’s advances grew by 14.7%

FII / NRIs / OCBs

32.9

yoy (1% qoq) aided by healthy retail loan book growth of 23% yoy. The main

Indian Public / Others

8.4

drivers leading to the growth in the retail loan book were personal loans/credit

card lending, which grew by 55%/33% yoy respectively. Retail contribution to total

loans increased to 61.4% vs. 57.5% in Q1FY2019. NIM stood at 3.62% against

3.72% in Q4FY19, considering 17bps impact of refund and interest collection of

Abs. (%)

3m 1yr

3yr

NPA. CASA ratio declined to 45.2% vs. 49.6% in Q4FY2019 as growth in term

deposits outpaced that in CASA deposits.

Sensex

(3.3)

0.9

33.6

ICICI Bank

8.7

46.3

73.4

Outlook & Valuation: At the current market price, the bank’s core banking

business (after adjusting the value of subsidiaries) is trading at 1.7x FY2021E

ABV. We believe strength of liability franchise (CASA - 45%), shift in loan mix

towards retail assets & better rated companies, strong capitalization (tier I of

14.6%), steady improvement in stressed loan and going forward quick resolution

under IBC would be the key triggers for expansion. We recommend a Buy on the

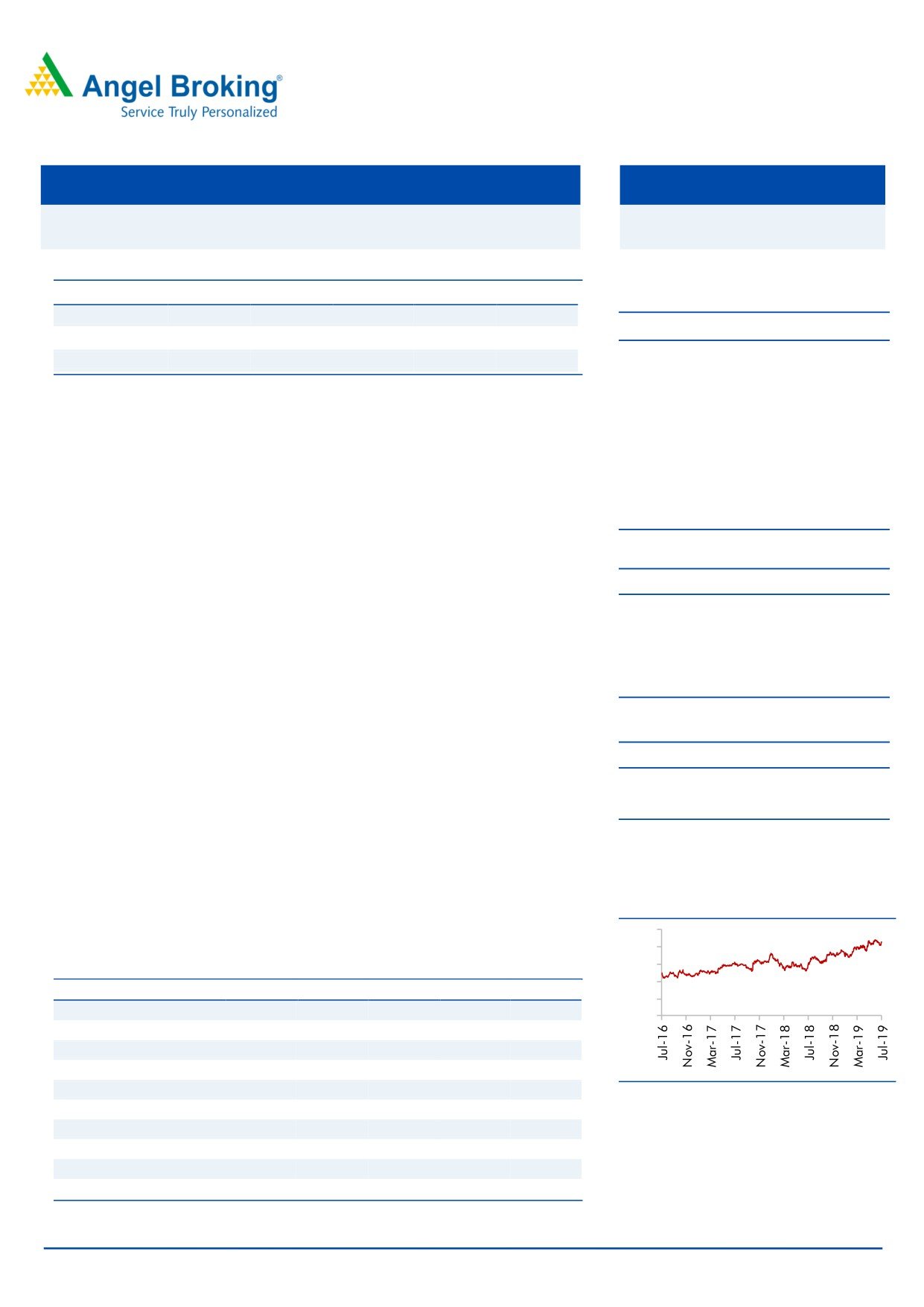

3 Year Price Chart

stock with a Target Price of `490.

500

400

300

Exhibit 1: Key Financials

200

Y/E March (` cr)

FY17

FY18

FY19

FY20E

FY21E

100

NII

21,738

23,025

27,015

31,732

37,135

0

% chg

2

6

17

17

17

Net profit

9,802

6,645

3,362

12,250

16,518

% chg

0.8

(32.2)

(49.4)

264

35

NIM (%)

3.2

3.1

3.2

3.4

3.5

Source: Company

EPS (`)

15

10

5

19

26

P/E (x)

28

42

82

23

17

P/ABV (x)

3.6

3.3

2.8

2.5

2.3

Jaikishan Parmar

RoA (%)

1.3

0.8

0.4

1.2

1.4

Research Analyst

RoE (%)

10.3

6.5

3.1

10.8

13.2

022 - 39357600 Ext: 6810

Source: Company, CMP as on 29/7/2019, Valuation done closing price of 29/7/2019

Please refer to important disclosures at the end of this report

1

ICICI Bank | 1QFY2020 Result Update

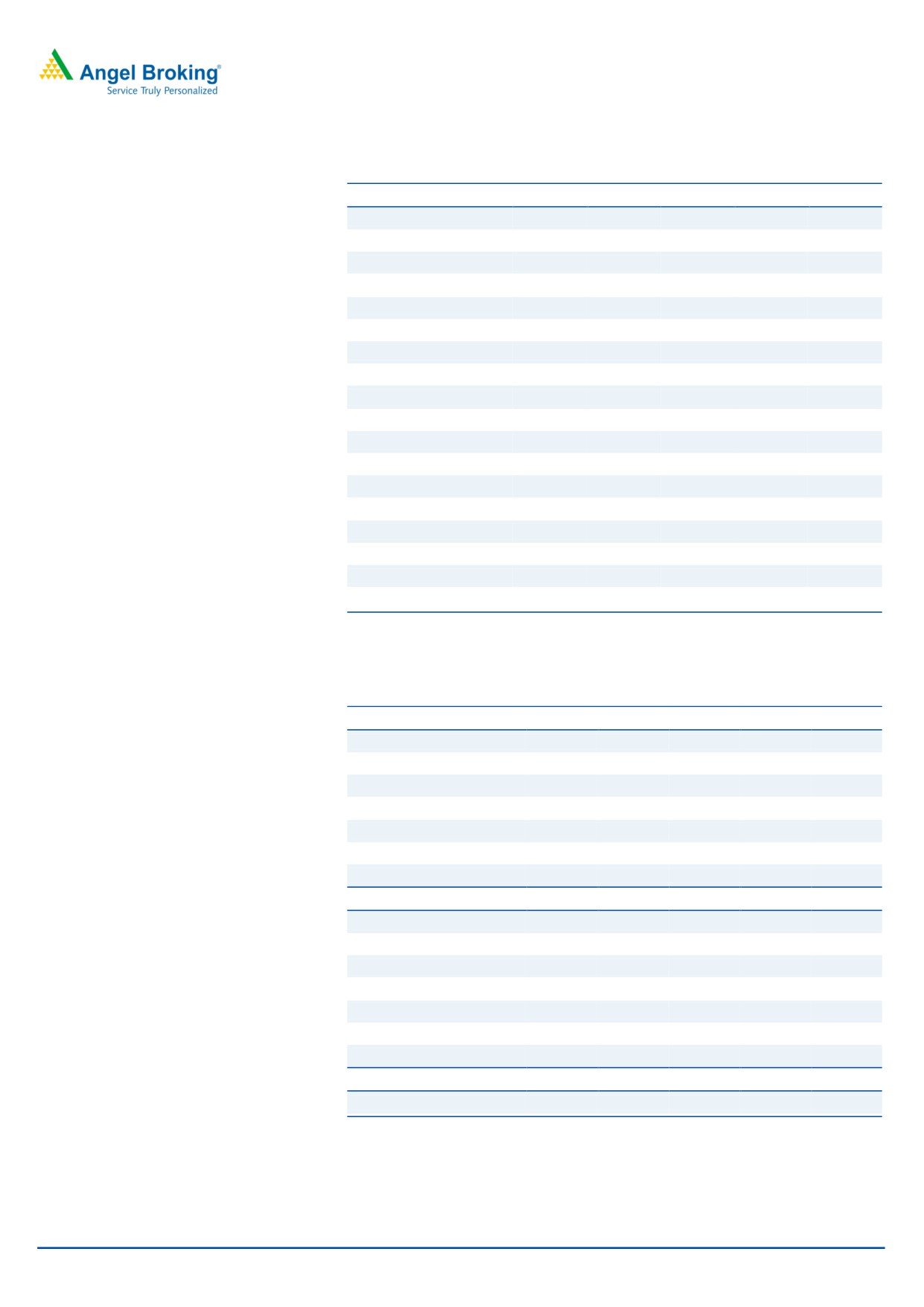

Exhibit 1: Quarterly Performance

Particulars (` cr)

Q 4FY18

Q 1FY19

Q 2FY19

Q 3FY19

Q 4FY19

Q 1FY20 % chg (qoq)

% chg (yoy)

I nterest Earned

14,264

14,722

15,106

16,280

17,293

17,980

4

22

on Advances / Bills

10,690

10,982

11,512

12,524

12,925

13,616

5

24

on i nvestments

3,001

3,136

3,086

3,237

3,338

3,645

9

16

on bal with RBI & others

166

227

147

135

227

147

(35)

(35)

on others

406

378

360

385

802

571

(29)

51

I nterest Expe nded

8,243

8,620

8,688

9,405

9,673

10,243

6

19

Net Interest Income

6,022

6,102

6,418

6,875

7,620

7,737

2

27

Non Intere st Income

5,678

3,851

3,156

3,883

3,621

3,425

(5)

(11)

Fee Income

2,755

2,754

2,995

3,062

3,178

3,039

(4)

10

Other Income

238

331

197

342

269

191

(29)

(42)

Treasury Income

2,685

766

(350)

479

156

196

26

(74)

Operating income

11,700

9,953

9,574

10,758

11,241

11,163

(1)

12

Operating Expenses

4,186

4,145

4,324

4,612

5,008

4,874

(3)

18

Empl oyee expenses

1,526

1,514

1,661

1,734

1,899

1,953

3

29

Other Opex

2,660

2,631

2,663

2,878

3,109

2,921

(6)

11

Pre-prov. profit

7,513

5,808

5,250

6,146

6,233

6,288

1

8

Provisions & Contingencies

6,626

5,971

3,994

4,244

5,451

3,496

(36)

(41)

PBT

888

(164)

1,255

1,902

782

2,793

257

(1,806)

Provision for Taxes

(132)

(43)

347

297

(187)

885

(573)

-

Tax rate

(15)

26

28

16

(24)

32

(223)

PAT

1,019

(120)

909

1,605

969

1,908

97

-

Source: Company

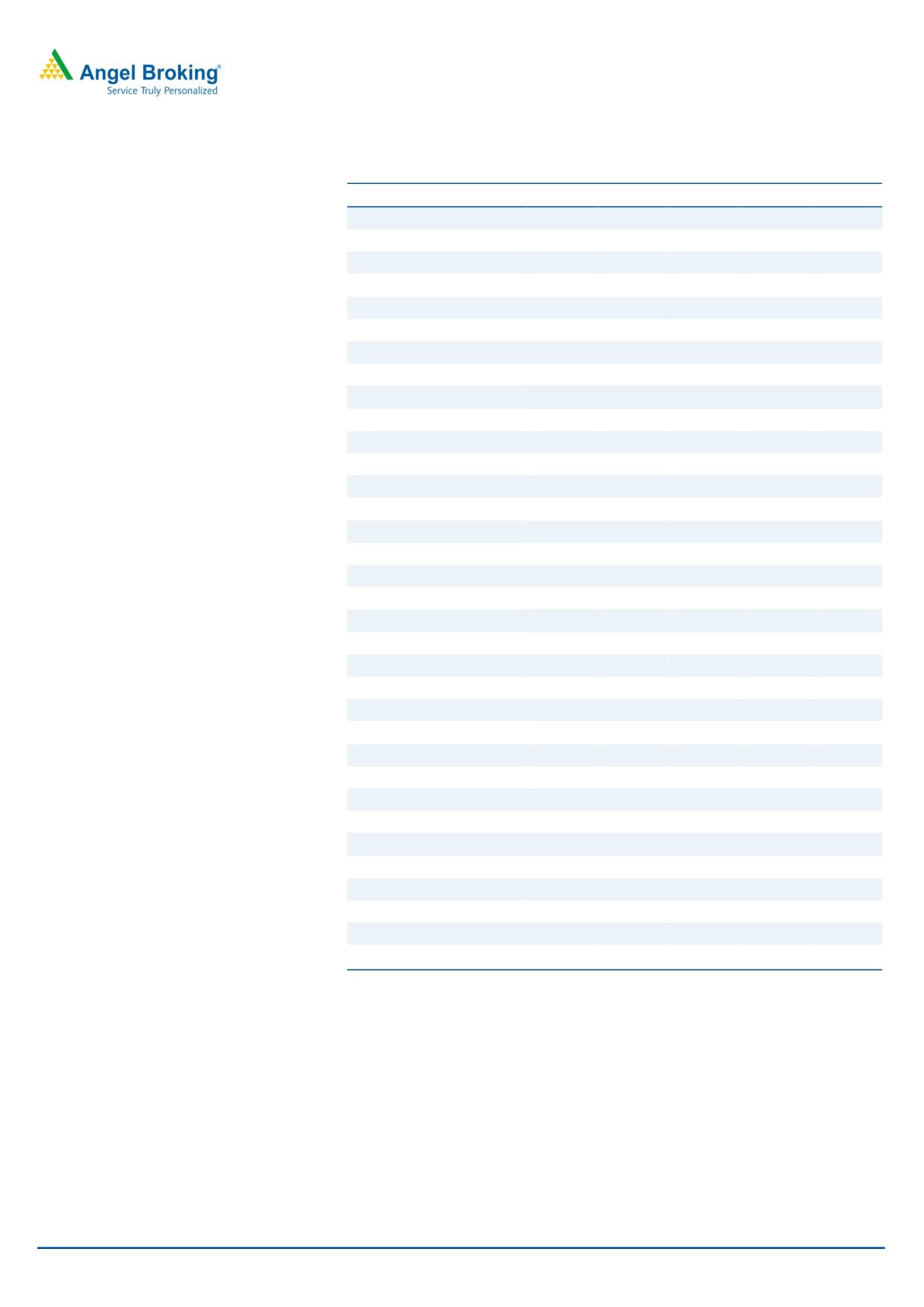

Exhibit 2: Balance Sheet

Particular

Q 4FY18

Q 1FY19

Q 2FY19

Q 3FY19

Q 4FY19

Q 1FY20

% chg (qoq)

% chg (yoy)

A dvance (` cr)

5,12,395

5,16,289

5,44,487

5,64,308

5,86,647

5,92,415

1.0

14.7

Deposit (` cr)

5,60,975

5,46,878

5,58,669

6,06,755

6,52,920

6,60,732

1.2

21

Credit-to-De posit Rati o (%)

91

94

97

93

90

90

(18.9)bp

(474.6)bp

CA (` cr)

88,958

76,689

76,072

88,581

96,269

80,401

(16)

5

SA (` cr)

2,00,967

1,99,604

2,07,476

2,10,793

2,27,671

2,18,476

(4)

9

CASA de posits (` cr)

2,89,925

2,76,293

2,83,548

2,99,374

3,23,940

2,98,877

(8)

8

CASA %

51.7

50.5

50.8

49.3

49.6

45.2

(438)bp

(528.8)bp

Tier-I ratio (%)

15.9

15.8

15.4

15.1

15.1

14.6

(49)bp

(124)bp

of w hich - CET1

14.4

14.4

14.0

13.7

13.6

13.2

(43)bp

(121)bp

Tier-II ratio

2.5

2.5

2.5

2.0

1.8

1.6

(21)bp

(92)bp

Total CAR ratio

18.4

18.4

17.8

17.2

16.9

16.2

(70)bp

(216)bp

Source: Company

July 30, 2019

2

ICICI Bank | 1QFY2020 Result Update

Exhibit 3: Profitability Ratios & Asset quality Trend

Particular

Q 4FY18

Q 1FY19

Q 2FY19

Q 3FY19

Q 4FY19

Q 1FY20 % chg (qoq)

% chg (yoy)

Rep. Yield on Advance

8.68

8.71

8.79

9.00

9.29

9.36

7bp

65bp

Rep. Cost of fund

4.93

4.99

5.00

5.14

5.20

5.23

3bp

24bp

Cost of De posit

4.79

4.81

4.76

4.88

5.00

5.08

8bp

27bp

Reported NIM

3.24

3.19

3.33

3.22

3.72

3.61

(11)bp

42bp

Cost-to-income ratio

35.8

41.6

45.2

42.9

44.5

43.7

(88.2)bp

201.7bp

Asset quality

Gross NPAs (` cr)

54,063

53,465

54,489

51,627

46,328

45,799

(1)

(14)

Gross NPAs (%)

8.8

8.8

8.5

7.8

6.7

6.5

(21)bp

(232)bp

Net NPAs (` cr)

27,886

24,170

22,086

16,288

13,613

11,893

(13)

(51)

Net NPAs (%)

4.8

4.2

3.7

2.6

2.1

1.8

(29)bp

(242)bp

PCR (%)

46

52

57

67

69

73

347.4bp

2028.7bp

Slippage ratio (%)

3.1

0.8

0.6

0.4

0.6

0.5

(13.6)bp

(31.3)bp

Credit Cost on Adv (Annl)

5.2

4.6

3.0

3.1

3.8

1.6

(218.9)bp

(304.4)bp

Source: Company

Exhibit 4: Stressed book on declining trend

Particular (` Cr)

1QFY18

2QFY18

3QFY18

4QFY18

1QFY19

2QFY19

3QFY19

4QFY19

Q 1FY20

GNPA

43,148

44,489

46,039

54,063

53,465

54,489

51,627

46,328

45,799

Outstanding stock of bad loans

28,300

28,300

25,800

13,461

11,898

10,720

3,690

3,299

3,280

(% of l oans)

6.1%

5.9%

5.1%

2.6%

2.3%

2.0%

0.7%

0.6%

0.6%

Stressed asset

Sub inve stme nt grade

20,400

19,600

19,100

4,728

4,401

3,283

Security receipts

3,400

3,500

3,400

3,438

3,438

3,436

3,299

3,299

3,280

Other dispensation

4,500

5,200

3,300

5,295

4,059

4,001

391

Restructured loans

2,400

2,000

1,800

1,595

1,445

1,443

391

...5.25

200

200

200

-

2,004

2,005

SDR

1,500

2,700

1,000

-

-

S4A

400

300

300

2,200

610

553

Other

1,500

-

BB & Below

17,100

18,812

17,525

15,355

Total Stresse d Pool

71,448

72,789

71,839

67,524

65,363

82,309

74,129

67,152

64,434

Stressed pool to loans (%)

15.4

15.1

14.2

13.2

12.7

15.1

13.1

11.4

10.9

Stressed pool declared as NPA%

60

61

64

80

82

66

70

69

71

Source: Company

July 30, 2019

3

ICICI Bank | 1QFY2020 Result Update

Outlook & Valuation: At the current market price, the bank’s core banking

business (after adjusting the value of subsidiaries) is trading at 1.7x FY2021E ABV.

We believe strength of liability franchise (CASA - 45%), shift in loan mix towards

retail assets & better rated companies, strong capitalization (tier I of 14.6%), steady

improvement in stressed loan and going forward quick resolution under IBC would

be the key triggers for expansion. We recommend a Buy on the stock with a Target

Price of `490.

Exhibit 5: SOTP

Valuati on

Value/share

Particular

%

Methodology

(`)

Value of ICICI standalone

100

2x FY21E ABV

383

Subsidi aries

ICICI Prudential Life

54.9

On Current Mcap

47

General Insurance

56

On Current Mcap

45

Mutual fund s

51

5.5% of current AUM

15

Other (Home Fin, VC, Securities

27

PD and Overse as subsi diaries)

Total subsidiaries' value @ 20% di scount

108

Fair value per share

490

Valuation done on closing price of 29/07/2019

July 30, 2019

4

ICICI Bank | 1QFY2020 Result Update

Income Statement

Y/E March (` cr)

F Y17

F Y18

F Y19

F Y20E

F Y21E

Net Interest Income

21,738

23,025

27,015

31,732

37,135

- YoY Growth (%)

2

6

17

17.5

17.0

Other Income

19,503

17,419

14,511

15,231

18,296

- YoY Growth (%)

27

(11)

-17

5

20

O perating Income

41,241

40,444

41,526

46,963

55,431

- YoY Growth (%)

13

(2)

3

13

18

O perating Expenses

14,754

15,704

18,089

20,327

23,402

- YoY Growth (%)

16

6

15

12

15

Pre - Provision Profit

26,487

24,741

23,437

26,636

32,029

- YoY Growth (%)

11

(7)

-5

14

20

Prov. & Cont.

15,207

17,307

19,661

10,055

10,005

- YoY Growth (%)

30

14

14

(49)

(0)

Profit Before Tax

11,279

7,434

3,776

16,581

22,023

- YoY Growth (%)

(8)

(34)

-49

339

33

Prov. for Taxation

1,478

789

413

4,332

5,506

- as a % of PBT

13

11

11

26

25

PAT

9,802

6,645

3,362

12,250

16,518

- YoY Growth (%)

1

(32)

(49.4)

264

35

Balance Sheet

Y/E March (` cr)

F Y17

F Y18

F Y19

F Y20E

F Y21E

Equity

1,171

1,292

1,294

1,295

1,295

Reserve & Surplus

98,780

1,03,868

1,07,074

1,17,377

1,30,591

Networth

99,951

1,05,160

1,08,368

1,18,673

1,31,887

Deposits

4,90,039

5,60,975

6,52,920

7,32,565

8,40,635

- Growth (%)

16

14

16

12

15

Borrowings

1,47,556

1,82,859

1,65,320

1,73,004

2,02,390

Other Liab. & Prov.

34,245

30,195

37,851

50,549

75,668

T otal Liabilities

7,71,791

8,79,189

9,64,459

10,74,790

12,50,580

Cash Balances

31,702

33,102

37,858

43,288

49,674

Bank Balances

44,011

51,067

42,438

33,128

38,015

Investments

1,61,507

2,02,994

2,07,733

2,35,682

2,72,942

A dvances

4,64,232

5,12,395

5,86,647

6,59,995

7,72,100

- Growth (%)

7

10

14

13

17

Fixed Assets

7,805

7,904

7,931

11,235

12,892

Other Assets

62,535

71,727

81,852

91,463

1,04,956

T otal Assets

7,71,791

8,79,189

9,64,459

10,74,790

12,50,580

- Growth (%)

7

14

10

11

16

July 30, 2019

5

ICICI Bank | 1QFY2020 Result Update

Key Ratio

Y/E March

F Y17

F Y18

F Y19

F Y20E

F Y21E

Profitability ratios (%)

NIMs

3.2

3.1

3.2

3.4

3.5

Cost to Income Ratio

36

39

44

43

42

RoA

1.3

0.8

0.4

1.2

1.4

RoE

10

6

3

11

13

B/S ratios (%)

CASA Rati o

50

52

50

47

49

Credit/Deposit Rati o

0.95

0.91

0.90

0.90

0.92

Asset Quality (%)

Gross NPAs

7.9

8.8

6.7

5.2

3.8

Net NPAs

4.9

3.5

2.0

1.6

1.1

Slippages

7.5

6.4

2.5

2.0

1.5

Loan Loss Prov. /Avg. Assets

2.04

2.10

2.13

0.99

0.86

Provision Coverage

40

48

71

70

70

Per Share Data (`)

EPS

15

10

5

19

26

ABVPS (70% cover.)

119

129

153

169

189

DPS

2

2

1

4

5

Valuation Ratios

PER (x)

28

42

82

23

17

P/ABVPS (x)

3.6

3.3

2.8

2.5

2.3

Dividend Yield (%)

0.5

0.5

0.2

0.9

1.2

DuPont Analysis

NII

2.9

2.8

2.9

3.1

3.2

(-) Prov. Exp.

2.0

2.1

2.1

1.0

0.9

Adj. NII

0.9

0.7

0.8

2.1

2.3

Other Inc.

2.6

2.1

1.6

1.5

1.6

Op. Inc.

3.5

2.8

2.4

3.6

3.9

Opex

2.0

1.9

2.0

2.0

2.0

PBT

1.5

0.9

0.4

1.6

1.9

Taxes

0.2

0.1

0.0

0.4

0.5

R oA

1.3

0.8

0.4

1.2

1.4

Leverage

7.9

8.0

8.6

9.0

9.3

R oE

10.3

6.5

3.1

10.8

13.2

Valuation done on closing price of 29/07/2019

July 30, 2019

6

ICICI Bank | 1QFY2020 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited, Bombay

Stock Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National Commodity &

Derivatives Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and Investment Adviser with

SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a registered entity with SEBI for Research

Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164. Angel or its associates has not

been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its

associates/analyst has not received any compensation / managed or co-managed public offering of securities of the company covered

by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document sho uld

make such investigations as they deem necessary to arrive at an independent evaluation of a n investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to de termine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other rel iable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any wa y

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this repo rt.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cann ot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduc ed,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may ari se from or in

connection with the use of this information.

Disclosure of Interest Statement

ICICI Bank

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

July 30, 2019

7